The purpose of this paper is to derive the optimal DOL (degree of operating leverage) of a company with flexibility in investment and production. The choice of DOL is a critical one because it impacts the company’s risk level, operating and financial performance, and valuation. However, there is virtually no research on how a company should choose its DOL. With a wide range of input parameter values, our model generates optimal DOL figures that are similar in magnitude to empirical estimates. We also identify the important determinants of DOL, such as costs (fixed cost, variable cost, and cost of capacity), demand characteristics (growth rate, volatility, and price-sensitivity), productivity of capital, and interest rate.

This allows investors to estimate profitability under a range of scenarios. As stated above, in good times, high operating leverage can supercharge profit. But companies with a lot of costs tied up in machinery, plants, real estate and distribution networks can’t easily cut expenses to adjust to a change in demand. So, if there is a downturn in the economy, earnings don’t just fall, they can plummet. Running a business incurs a lot of costs, and not all these costs are variable.

Difference between Operating Leverage and Financial Leverage Accounting

In evaluating the wisdom of their investment in a corporation, its owners

should use the current market value of its stock, because this is what they would have

available to invest elsewhere if they liquidated the stock. This team of experts helps Finance Strategists maintain the highest level of accuracy and professionalism possible. The articles and research support materials available on this site are educational and are not intended to be investment or tax advice. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

What does operating leverage depend on of a firm?

Significance. Operating leverage calculation measures the company's fixed costs as a percentage of its total costs. Therefore, a company with a higher fixed cost will have high operating leverage than a higher variable cost.

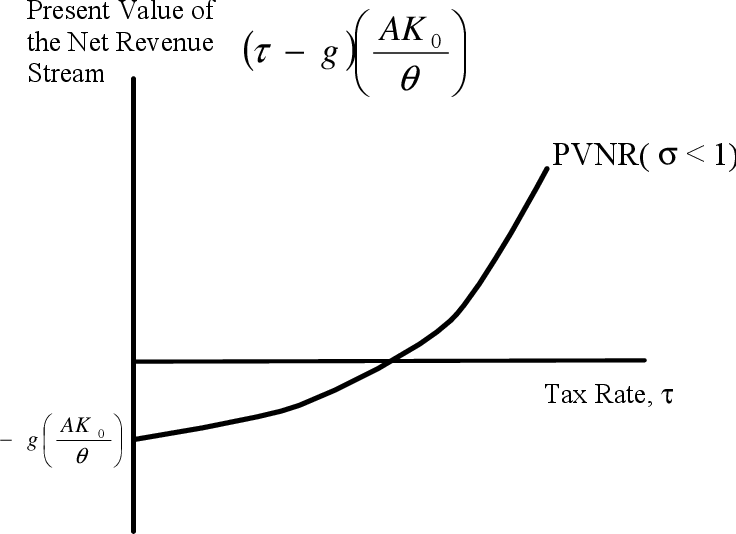

Therefore, what is missing in the literature is a comprehensive model that determines DOL in a joint production/investment framework. Moreover, we also consider the effect of demand behavior and uncertainty (which impact DOL via the output price and quantity choices), by means of a stochastic downward-sloping demand function. Kumar and Yerramilli (2016) examine the relationship between operating and financial leverage, using a real-option model where the firm jointly identifies optimal capacity and optimal leverage ratio. They show that optimal DOL is an increasing function of cash flow volatility if the cost of subsequent expansion is high enough. However, their DOL is completely determined by capacity (in fact, capacity is treated as interchangeable with DOL), hence the other determinants of DOL are ignored.

Irreversibility and aggregate investment

It is widely recognized that the DOL has a significant impact on a company’s operating and financial policies and performance, thus it is necessary to choose the DOL judiciously. However, the existing literature focuses on the effects of DOL, and not on the choice of DOL. While a few papers have studied the firm’s DOL choice, they ignore either the investment (capacity and timing) decision or the production (output level) decisions, both of which are crucial in determining the DOL. Unfortunately, unless you are a company insider, it can be very difficult to acquire all of the information necessary to measure a company’s DOL. Consider, for instance, fixed and variable costs, which are critical inputs for understanding operating leverage. It would be surprising if companies didn’t have this kind of information on cost structure, but companies are not required to disclose such information in published accounts.

In this article, we’ll give you a detailed guide to understanding operating leverage. Generating this type of cost information is very different than the requirements of GAAP. Accountants try to create management information that links to GAAP; but since cause and effect is not a GAAP principle, the effort is doomed to fail. The only way to generate causal information on the nature of costs is to apply resource consumption accounting or a German management accounting method known as grenzplankostenrechnung (GPK for short). Activity-based costing has a tendency to make all costs appear variable and should be used with caution to ensure the fixed and variable nature of costs are accurately reflected. In spite of its importance, there is surprisingly little research on how a firm should decide on its DOL; in other words, what is the company’s “optimal” DOL?

Why You Can Trust Finance Strategists

Owners’ return rises by 9.33 percent as a result of the financial

leverage obtained by 70 percent debt financing at a cost of 8 percent. If borrowing rose

above 70 percent, this figure would rise, that is, financial leverage would be greater. If

financial leverage is measured, instead, as an index number, an additional calculation is

necessary to determine what return on equity it produces. Businesses change the level of output in order increase the rate of return

enjoyed by their owners. This can be done either by selling more units or avoiding

producing units which cannot be sold without a rate-of-return-reducing reduction in price.

- Shown in Tables

1 and 2 (below) are their revenues and costs for the production of up to 25,000 units of

output. - The value of this ratio is greater the lower is the ratio of variable cost

per unit to price per unit; so, the greater is this ratio, the higher is operating

leverage. - Insourcing provides the options to reduce the fixed cost structure (the reduce FC option), reduce the variable costs (the reduce VC option), or reduce both through process improvement, innovation and investment.

- The management of ABC Corp. wants to determine the company’s current degree of operating leverage.

- Higher DOL means higher operating profits (positive DOL), and negative DOL means operating loss.

This information shows that at the present level of operating sales (200 units), the change from this level has a DOL of 6 times. This variation of one time or six-time (the above example) is known as degree of operating leverage (DOL). It is also useful to frame this as the operating margin, which compares the overall revenue to the overall

operating income.

Similar to Types of Leverage(

As sales took a nosedive, profits swung dramatically to a staggering $58 million loss in Q1 of 2001—plunging down from the $1 million profit the company had enjoyed in Q1 of 2000. During the 1990s, investors marveled at the nature of its software business. The company spent tens of millions of dollars to develop each of its digital delivery and storage software programs. But thanks to the internet, Inktomi’s software could be distributed to customers at almost no cost.

However, increasing operating leverage can also cause substantial losses

and puts more pressure on a business. The key to understanding the appropriate amount of operating

leverage lies in the analysis of the break-even point. In finance, companies assess their business risk by capturing a variety of factors that may result in lower-than-anticipated profits or losses. One of the most important factors that affect a company’s business risk is operating leverage; it occurs when a company must incur fixed costs during the production of its goods and services.

Fixed costs do not vary with the volume of sales, whereas variable costs vary directly with sales volume. When sales have exceeded the break-even point, a larger contribution margin will mean greater increases in

profits for a company. By inserting different prices into the break-even formula, you will obtain a number of

break-even points – one for each possible price charged. The value of this ratio is greater the lower is the ratio of variable cost

per unit to price per unit; so, the greater is this ratio, the higher is operating

leverage. Block and Hirt’s method produces the

same results when operating leverage is computed at the 10,000 unit level of output. Although you need to be careful when looking at operating leverage, it can tell you a lot about a company and its future profitability, and the level of risk it offers to investors.

More sensitive operating leverage is considered riskier since it implies that current profit margins are less secure moving into the future. Unit contribution margin can be thought of as the fraction of sales, or the amount of each unit sold, that

contributes to the offset of fixed costs. Operating leverage exists when a firm has to pay fixed cost irrespective of volume of output or sales. operating leverage arises because of An even more extreme case is produced by letting Widget Works, Inc. have

fixed costs of $10,000 and variable costs per unit of $1.00, while Bridget Brothers has

fixed costs of only $100 and variable cost per unit of $1.99. Observe that now Widget

Works’ fixed costs are 100 times Bridget Brothers’, and that its variable costs

are just barely over one-half of Bridget Brothers’.

What does operating leverage depend on of a firm?

Significance. Operating leverage calculation measures the company's fixed costs as a percentage of its total costs. Therefore, a company with a higher fixed cost will have high operating leverage than a higher variable cost.